Braemar PLC: Setting Sail to Sweeter Seas

Braemar PLC: Setting Sail to Sweeter Seas

CEO Gundy has positioned Braemar for sustainable growth. Shipping conditions are buoyant and 7x PE will prove too low. My 12 month fair value target is 475p, 75% total return (70% capital, 5% divY)

Summary

I forecast rich returns for shipbrokers in 2024 and 2025 as the market starts to grapple with a structural weakness in the supply side of the Tanker market and newfound momentum in Dry Cargo as the interest rate environment abates. With this backdrop, UK shipbrokers Clarkson and Braemar will be poised to deliver additional good years of revenue and profit growth. Braemar combines this thematic trade with a real self improvement story. It has de minimis exposure to the third big shipping market of containers, which has supply side overcapacity and where rates will remain low in 2024. Further to this, it is trading at a large discount to my perceived 475p fair value, to its closest peer Clarkson (13x PE, Clarkson’s own norms 18x+ PE), and to Braemar’s own long-term norm valuation levels.

Under the new CEO James Gundy, Braemar is now streamlined and on a sustained growth path. There is a real sense the company now has its act together with a real growth mentality. Compared to years back when Braemar was heavily indebted, the now transformed balance sheet provides ammunition for Braemar to sustainably grow revenue and profits. With greater revenue diversification, the company target remains “not less than £18m from FY25 onwards.” For Braemar because they are a February financial year end business, FY25 starts next February. I am bullish on the shipping rate outlook and Braemar’s own growth opportunities and expect normalized profit after tax of £14mln next year.

5 years ago, Braemar was a stock I’d only dare to ‘rent’. Now, it is one that can be ‘owned’, with a combination of a thematic trade (shipping strength and tanker shortage) and an idiosyncratic stock trade (cheap valuation, self-help and a move to sustained growth). Chartering is at the business core, but investors are overlooking the growth story in Braemar Securities. This has evolved rapidly from £3mln to £17mln of revenue in only 3 years, and it looks capable of reaching £50mln of revenue in the next 5-7 years.

In the short run, broker forecasts look too low, with Dry Cargo conditions significantly picking up right since the turn of the second half of the year (see the Baltic Dry Index which has soared in recent weeks). Conditions in other Chartering areas should remain strong according to time charter rates, and Risk Advisory should continue growth apace. I forecast £158mln of revenue for this financial year compared to broker averages at £150mln.

I forecast Braemar to generate £13.5mln+ of FCF in FY25, and on my forecasts Braemar is only on a 6.8x Y+2 PE and 6.0x Y+3 PE. My fair value is 475p/sh which would put the company on a Y+2 PE of 10.2x and give a 75% total return (capital return and dividends). I think we will see Braemar as a 10-12x PE corridor stock again. Shareholders will have also received meaningful dividends, starting with 12p worth that go ex-dividend in January/February (4%+ return). The next update should come in February with the full year trading statement. My stretch fair value is 660p, my ‘it went wrong’ fair value is 200p.

Link to Cavendish Research on Braemar if you classify as a sophisticated investor and sign up

Link to Edison Group Research on Braemar

Calendar dates to watch out for

4 January 2024, ex-dividend date on 8p final dividend in respect of FY23

23 February 2024, ex-dividend date on 4p interim dividend in respect of H1 FY24

Middle February 2024, pre-close trading update

The swashbuckling world of Shipbroking

According to the OECD, ~90% of traded goods are carried over the waves, making it the main transport mode for global trade. It is also the most environmentally efficient transport mode.

For all of the lights of its financial districts or factories in its manufacturing heartlands (long diminished perhaps), one industry that Britain has dominated for decades is shipbroking, with London the shipbroking heart.

As the UK Institute of Chartered Shipbrokers puts it, “Archives in the City of London dating back to 1285 assert that "there shall be no brokers in the City except those who are admitted and sworn before the warden or Mayor and Alderman". The privilege of a licence to trade was granted to a broker for an annual fee of £5 and the promise that he would abide by certain rules to ensure he would behave in an honourable fashion: any misdemeanours were answerable to the Court of Aldermen. This system lasted for an extraordinary six centuries, giving rise to the term 'Honest Broker'.

In the realm of shipbroking, cultivating relationships is integral, mirroring the interconnected nature of the entire shipping sector. On the chartering side, a key activity, a shipbroker’s job is to introduce, structure and manage contracts to agree commercial terms between shipping principals (the ship owner or operator) and the customer who wants their cargo shipped). In the real world that means sourcing ships to carry the cargo, finding one that is available at the right time, with the right counterparty, at the right price. Shipbrokers are normally involved in chartering (organising the transport of cargo) and sale & purchase (organising the sale and purchase of ships, both new and second-hand).

Knowing who is on the other end of your transaction is paramount. The last thing you want is to transact with an ill-intentioned counterparty and an important role of a broker will be to ensure that does not happen. In an increasingly globalised world, the sign of a good shipbroker is one who reduces risk for both counterparties, but being a verifying intermediary. As it did three centuries ago, shipbroking continues to be a crucial component in powering the engine of the shipping industry.

The shipbroker ‘fixes’ a deal when agreement is reached. A saying in the industry is that ‘you should not fix and move on’. The broker still has a roll even after the fix is reached, making sure there are no further problems in the lifecycle of the transaction. At the end of the day, commissions are only paid when there is a successful fixture. Similar to numerous brokerage positions, shipbroking is an industry where shipbrokers often work long hours and it is not a 9 to 5 role. There is a typical large bonus percentage of overall shipbroker employee compensation.

It has not all been smooth sailing for Braemar shareholders. The stock was suspended for many months this year while specialist forensic accountants FRP audited the books from 2006 to 2013, focusing on some specific transactions, and settling on a legacy £2mln provision to reflect the concerns. Ship-tight compliance is not quite how the industry always operates, and firms will run into murky waters from time to time, but firms will continue to professionalise standards around this (and take fines where they don’t). For now, client entertainment is a real expense, and broking firms must maintain industry reputation for quality of service in a competitive market.

Braemar split their shipbroking activities into a few areas:

Chartering (70% of revenue); Building long term relationships between shipowners and charterers, to help manage the flow of transactions across shipping, and providing technology and databases to make this process smoother. On smaller ships, Braemar gets 2.5% of the revenue of the freight, on bigger ships it is 1.25% (a global standard level that has lasted for over a century).

Investment advisory (17% of revenue); Helping the shipping industry make careful and informed decisions, with an industry that is evermore focused on risk, and environmental regulations. IA includes investment consultancy, sales & purchase brokerage (broking the sale and purchase of new and second hand ships), asset valuations, recycling/end of life processes, and corporate finance advisory.

Risk Advisory (13% of revenue); Helping clients protect against turbulence in price movements and cyclical liquidity crunches that are common in shipping. RA includes derivatives brokerage (using Braemar Screen, the first bespoke trading technology tool for FFA derivatives), loan restructurings and carbon offsetting brokerage. On the derivatives activity with maritime futures contracts, Braemar is not taking any principal risk.

A world of change and consolidation

The shipbroking world has not been scared of consolidation and change. Clarkson has been the industry mainstay and with a hint of irony, it was a fragment of the Clarkson tanker team that left in 1983 that led to the creation of Braemar. Braemar today was then the result of a merger in 2001 between Braemar and Seascope Shipping, and later on ACM Shipping. Other players have done M&A too. Clarkson bought RS Platou, Howe Robinson acquired ICAP’s business unit, and last year there were rumours that Clarkson were interested in Maersk Broker.

Over time the larger houses have gotten bigger as they have extended their capability set, and as they have proven the best at weathering the usual churn and turn of particular brokers or broker teams leaving to competition or set up their own house. The credibility of a big broker, the scale and broad scope of their offerings are all sustaining competitive advantages, but the industry remains highly structurally fragmented.

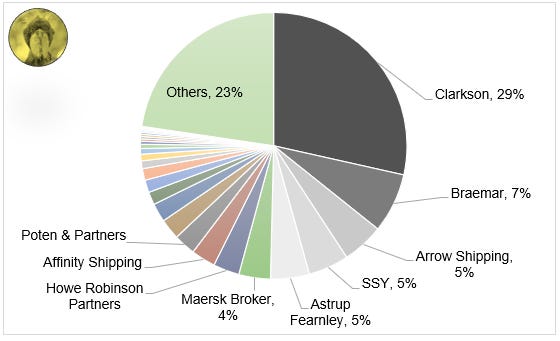

There is a dearth of proper market research on the shipbroking sector, so I took the time to scrawl through company reports and subsidiary reports to create a bespoke look at the shipbroking sector market share picture. Clarkson is by far the market leader, at I estimate a 29% market share, Braemar is the number 2, and other bigger players are such as Arrow, SSY and Astrup. Braemar has 17 global offices, and more than 400 staff across the globe.

Clarkson has outperformed most listed UK companies, demonstrating the sector attractiveness when combined with top tier management

Such is the impressiveness of Clarkson’s history of growth and profit improvement, the stock which is now at 2,950p has been a better performer since its inception than most listed companies today. Clarkson has generated a lifetime return since 1988 of nearly 1,800%. This overshadows almost every UK listed equity, including some of the UK’s top notch operators;

Astrazeneca’s 1,582% return since 1993

Rio Tinto’s 1,240% return since 1989

Relx’s 1,168% since 1989

Reckitt Benckiser’s 1,103% return since 1989

Unilever’s 962% since 1989

The Braemar deterioration (2015-2018) and the Braemar rejuvenation (2020+)

Going way back to start, Braemar in 2015 was the amalgamation of several companies: Cory Brothers, a logistics and shipping agency, original Braemar, Seascope, ACM Shipping, and engineering arm Wavespec. Up until 2015 the stock was a high flyer, with great returns for investors. However, from 2016 onwards, things started to deteriorate.

Braemar had just ended a fantastic FY16 (to the end of February 2016). Revenues had climbed 9%, EPS 8% and net cash was over £9mln. However, in 2016 Braemar was a predominantly tanker focused shipbroking house. Deep sea tankers constituted 48% of revenue, so the company was not well diversified. That market was set up to weaken over the year, while the Wavespec engineering division was hurt by oil and gas downturn that crushed capital expenditure in the sector. This led to a row of profit warnings and a derailed growth story.

Things were getting back on track in 2017 as the market rebounded and Braemar was putting in a stronger than expected performance in shipbroking. But then it was the turn of Braemar’s previous management to snatch defeat from the jaws of recovery. Braemar made an ill-fated acquisition that then weighed on the company for years afterwards. The acquisition of Naves Corporate Finance in September 2017 for a maximum of €35mln. Naves ended up underperforming expectations in a weak transaction environment while net debt across the business climbed as operating profit in the business shrank. Current CEO James Gundy would later acknowledge that Braemar overpaid for Naves and maybe did not do enough due diligence on the deal.

By the end of FY20, Braemar was generating only £9.6mln of underlying operating profit (compared to £13.8mln in FY16 and with Naves which should have taken this number to £17mln), and was running with over £40mln of total net debt and contingent consideration liabilities. All in all, the high flyer years of revenue and profit growth had unwound through questionable management decisions. The M&A had left Braemar’s balance sheet severely weakened too. Throwing everything into the mix, Braemar’s valuation multiple fall at the time was very justified.

The Simplification and Rejuvenation

James Gundy stepped into the CEO seat on January 1st 2021 having been the head of the main shipbroking activities of Braemar. He inherited a business that was lost for direction and with a share price of 150p. He was not completely on his own with turning Braemar around as serial turnaround specialist and Chairman Ronald Series had been working on the project for 18 months. But Gundy knew the industry and where Braemar should focus. The strategy involved divesting activities where Braemar was not carrying real specialism or understanding.

Much of the simplification that Braemar went through was in 2021 and 2022. The non-exhaustive list included the incident response business to Brazilian Grupo Ambipar, the sale of the offshore, marine and adjusting business to Aqualis, and then the sale of Braemar’s stake in AqualisBraemar LOC, the sale of Wavespec (a loss making engineering division), restructuring of payments from a past acquisition of Naves, and the disposal of the logistics division, Cory Brothers.

What was left was a much cleaner core around shipbroking and ancillary activities, returning Braemar' to its historical strengths and also its most profitable parts. The other key was improving the revenue mix in shipbroking, building out resilience by diversification. By FY23, deep sea tankers had reduced 28% of revenues, compared to 48% in FY16, but that was by growing the rest of the group not by shrinking tankers. Shipping markets do not all move in tandem so this much better mix of revenues provides a crucially more resilient and diverse revenue and profit pool for Braemar today that supports their £18mln+ profit target whatever the shipping weather.

Peel back the onion and Braemar is a much better growth business than it appears

On face value, Braemar’s group revenue performance since 2013 has not been that endearing as revenue has bounced normally between £120mln and £150mln. Though peel back the onion and just looking at shipbroking, finance and risk, and take away the previously plagued (and sold) Technical, Logistics and Engineering ventures and there is a much more endearing upward trend.

A hidden high growth business. Braemar Securities has quadrupled revenue since FY21

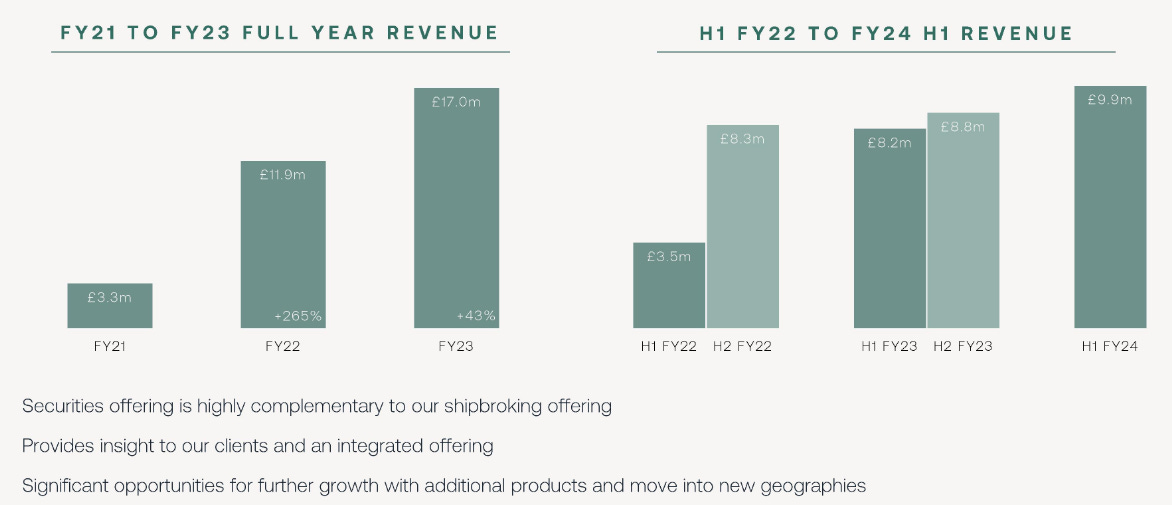

The strategy has also involved developing and bulking out ancillary services for chartering, like Braemar’s Securities offering which has quadrupled over the last 3 years to >10% of revenues, growing from £3.3mln in FY21 to £17mln in FY23 and growing a further 20%+ in the first half of FY24. This is a major opportunity for Braemar, with the securities business really only present in the UK at the moment, but which is a platform that can be rolled out more globally over time. The EU ETS regulation changes coming soon will an additional stimulus to growth, by further allowing Braemar to provide a service for shipping clients to manage the physical purchase of carbon credits in the EU. It would not be surprising to see Securities as a close to £50mln revenue business within 5 to 7 years. I asked Braemar this exact question on their half year presentation call with retail investors: can Securities get to £50mln in 5-7 years? Their answer was that their opportunity set in the UK, Europe, Singapore and other countries can support that ballpark number.

“Our proven future-facing strategy is delivering sustainable profit and growth, progressive dividends”

The strategy now is to grow organically but to add new geographic and technical capabilities on top of that, a dramatically lower risk strategy than before. In FY23 that involved acquiring two new tanker desks (in Madrid and Florida), launching new natural gas and oil derivatives desks, and opening a corporate finance desk in Athens. Outside of growing shipbroking breadth and market share, other strategic priorities are on developing technology solutions through Braemar’s digital transformation programme, and continuing to build the Braemar brand.

A people business at heart

To readers who have read this far it will come as no surprise that shipbroking is a people and relationships service business. As such, company culture and workplace dynamics are as important as any financial metric we may look at when evaluating a company.

Besides my own research, it is encouraging that these soft factors are heading in the right direction. Chairman Nigel Payne summed things up nicely in November: “Over the past year, the Group continued to invest in its people. We expanded our teams across the globe, implemented new programmes to attract and retain top talent, and our strong performance is due to their hard work and creativity. As a result of their successes, the Braemar brand continues to rise. This is now beginning to create a virtuous circle, in which, as our reputation grows, we are better able to attract high performers, who further enhance Braemar's performance, working environment, brand and overall client offering to the benefit of all stakeholders. There is a renewed energy within Braemar, and the business is in a good place.”

Braemar is also taking the right steps to ferment the next generation of shipbroking talent, after launching their inaugural trainee shipbroker scheme in London in FY23.

Shipping outlook. Favourable conditions are here to stay

A macroeconomic recovery and Panama Canal disruption the upside wildcards to an attractive tanker supply crunch story

World trade is a traditional GDP activity, growing 2-4% per annum. The global GDP outlook into 2024 is for another year of growth. The IMF forecasts growth in 2024 of 2.9%, a shade under 2023 at 3.0%, and down on 3.5% in 2022 and 3.8% which was the 20-year average before the coronavirus entered the frame.

Surely low container shipping rates present a bleak outlook for sector and Braemar, right? No. Containers are only one type of shipping category. Braemar’s revenue mix is predominantly exposed to Tankers and Dry Cargo, with no real exposure to the container segment. That is good news, as the container segment remains oversupplied after the pandemic shortage spurred new capacity and it is sensible to assume container rates stay under the cosh.

Putting the individual tanker and dry cargo conditions to one corner, events in the Panama Canal have been going under the vision of much of the economic world. Finally late in November, market commentators started to recognise what shippers have been talking about for months. Drought conditions around the canal have dramatically reduced the number of shipping vessels that can pass through the canal; from next February, the canal capacity restrictions will allow throughput at only 45% of normal levels. That is already causing ships to shift and route through any of the Suez Canal, Cape of Good Hope or the Strait of Magellan, adding hundreds or thousands of miles to their journeys and driving up shipping rates. See this Glencore ship example just weeks ago, which routed thousands of miles astray in order to avoid disruption at Panama. It is expected that a traffic increase will only be possible in the middle of 2024 when the rainy season recommences. Panama could well continue to strongly support Dry Cargo rates for for the next 6 to 9 months.

Tankers - An incoming supply crunch will be very rates supportive

The conditions for Braemar in tankers is bright, and has been bright for much of the past year or two. These are not only cyclical factors.

Yes, oil demand has proved resilient (and the IEA bumped their demand expectations again in November), but let us not forget that the Russia-Ukraine was has remapped tanker trade routes to shippers advantages (and that will probably be true for the foreseeable future). Russian sanctions have prompted a significant increase in shipping mileages; Clarkson have highlighted how global seaborne trade ton-miles will have grown almost 7% 2021-2024 compared to trade tonnes up 4.5%. There is also a dark fleet of ships solely serving Russian crude and exports, which has taken vital capacity out of normal trade routes and may account for 10-12% of the global tanker fleet. Changes in Russia sanctions do not appear on the agenda, keeping longer seaborne distances in play next year. Oil products have been the main impacted by this, as Russia push oil out to China and India instead of the shorter journey to Europe. With irony, Braemar and shipbrokers probably benefit from many acts of god or war.

Tanker supply dynamics are also tight with the order book for new tankers still limited, and build times meaning any new orders will only come in 2027 and so higher capacity may be more a 2027 story at the earliest. ING point out that the tanker order book level in 2023 reached its lowest level for more about 30 years. Consider that a new-build tanker may have a 20 year operating lifecycle, and a significant number are at or close to surpassing this threshold. Tanker fleet growth is expected to be nigh on zero for the next few years according to Clarkson data based on the orderbook and conservative recycling estimates. As Gibson point out, the tanker orderbook compared to the number of vessels over 15 years in age is a fraction of where it should be, because of years of underinvestment. This matters because of the long lead times on building new tankers.

If you look at the order book data from Fearnresearch, the order book deliveries over the next few years are minimal and are particularly thin in VLCCs. Shipyards are at full capacity and are focused on higher margin segments of LNG, Containers and LPG, with the number of large yards capable of 20k+ dwt vessels down 60% since the 2009 peak. We really are in the world of a tanker shortage and that will become more headline news over 2024 and 2025. In my eyes, 2024 will be a year of very supportive tanker rates for the market and Braemar.

This will prompt higher second-hand tanker prices, which we are seeing, and also helping shipbrokers’ sale & purchase activities into next year (VLCC newbuild costs are at the highest levels since 2008). Teekay Tankers, a large US operator of mid-sized vessels has this to say about the supply factors: “Spot tanker rates have firmed significantly through early Q4-23, while positive long-term fleet supply fundamentals point to continued strength over the next 2 to 3 years.” A view shared by Scorpio, Hafnia amongst other market players.

Rising ton mile demand

One demand trend that will not be fading soon is the structural trend for higher oil demand growth to be coming out of the Asia Pacific region, but for the energy production to be mostly in the Western World (North America, Latin America). Because of this disconnect, Hunter Group estimate that a 1mln barrel per day increase in US production would necessitate the use of 56 VLCCs while an OPEC+ cut of this magnitude would only reduce VLCC demand by 24. Scorpio Tankers point out that 2024 tanker fleet growth will be only 0.5% against an expectation that ton mile demand may grow almost 7%.

All of these factors support higher tanker rates and higher shipbroker tanker profits for longer.

On the negative angle, OPEC+ have agreed to extending oil production curtailments into early 2024 to support oil prices, and this takes oil off tankers. However, I do not expect this to really depress tanker rates and it has not so far because of surging production in the US and outside of OPEC+, for export, and the supply crunch. I would add that OPEC+ compliance levels with the cuts may not end up being as high as the alliance hopes for. Jefferies also state that production outside of OPEC+ is expected to increase 1.2mln barrels a day between April and September 2024, and any unwind of OPEC+ curtailments would add further cargo demand onstream.

Looking beyond traditional products into specialised tankers like LPG/LNG, the outlook is positive, and Russia sanctions may play a future part too: Gas carrier chief predicts higher rates for natural gas freight if ongoing EU negotiations end with restrictions on Russian LNG imports. The Baltic Dirty Tanker index is a valuable insight and levels have stepped into a higher range. The index has climbed off summer lows in September, October and November to stand at 1,167. If you look at the x axis these are very supportive rates compared to most of the post financial crisis era.

Very Large Crude Carrier (VLCC) rates are also at very healthy levels and I expect this to stay this way if not even improve over 2024 as the tanker supply crunch becomes even clearer.

Dry (Bulk) Cargo - 2023 downcycle ending with a bang

2023 has been quieter on the Dry Cargo front as macro conditions have been quiet and these activities are impacted by activity levels in the global manufacturing and industrial industry. Therefore rates across the side spectrum (Panamax, Supramax, Handysize) were worse for wear in 2023 compared to a more active 2021 and 2022, and Dry Cargo was a drag for Braemar in its first half.

But from here the outlook into 2024 looks more positive. Take an example; iron ore and coal is heavily reliant on the market in China, and recent China stimulus packages have supported an improved forward outlook. See iron ore prices which have reached $133/t in recent weeks compared to $105/t in the Summer. The panama canal capacity restrictions are too mainly impacting Dry Cargo vessels, provided further support. This positive view is echoed by Lloyd’s list who also point out that dry cargo demand is anticipated to grow 4.4% next year compared to 2.5% fleet growth (another demand supply side imbalance).

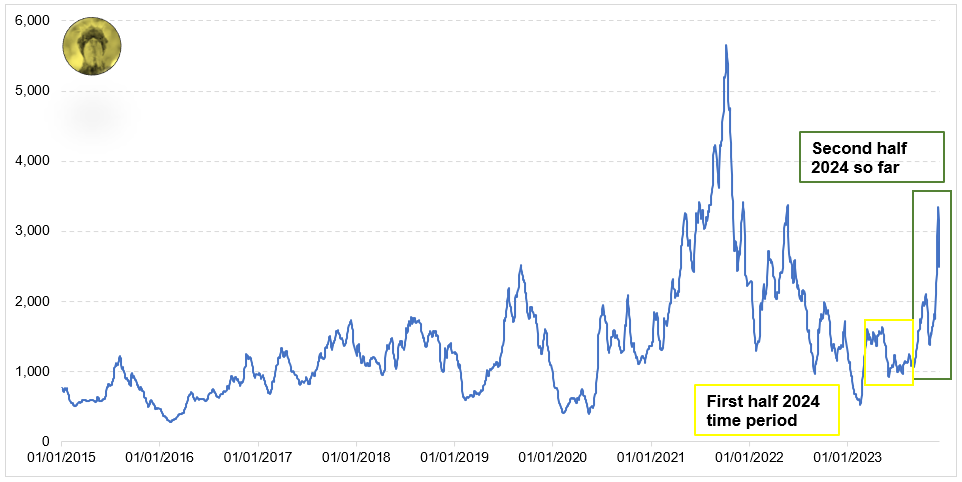

The Baltic Dry Index is your vision into the Dry Cargo market, and as the demand outlook has abated, conditions in the BDI readings too have been improving since the Summer lull, with the index soaring up to a reading of 3,000. China stimulus and the impact on demand for iron ore (and shipments on better weather) have been one of the many reasons boosting sentiment. As a rule of thumb, if the Dry Cargo market can hold above 2,000 never mind the ~2,500 it is at or 3,300 it recently got to, then Braemar’s Dry Cargo business is going to enjoy an upswing.

1st half of 2024 results

These were never going to be the spectacular results to get the share price moving, as Braemar put in place the cost foundations to drive future growth and as US dollar effects played through the margin. None the less, revenue growth of 8% to £74.9mln, fixtures growth of 8% (volume) was impressive, even as underlying operating profit excluding FX movements shrank from £8.9mln to £7.5mln. Fully underlying operating profit was £8.4mln compared to £8.9mln in the previous year. Underlying EPS was 17.43p. Net cash was £3.1mln (and has increased to £5.3mln at the end of September).

On the outlook, Braemar said market conditions were healthy, the order book had risen to $65.6mln at the end of October, and that the group is on track to both meet FY24 market expectations and the target to double underlying operating profit by FY25.

Broker Cavendish held their forecasts for £151mln of revenue and 38p of EPS for this year, although they acknowledge that these are conservative, and I think that is true especially so on the revenue line. In the first half the area of strength were broad in chartering, but there was a weaker Dry Cargo market (revenues -37% yoy). Nothing surprising given market conditions, but take into consideration that Braemar’s first half was from the start of March 2023 to the end of August 2023. Then compare that to what has happened to the Baltic Dry Index since September 2023, and it will become clear how this should be a much better performance from Dry Cargo and the whole group in the second half of the FY24 year and into FY25. Zoom out on the BDI chart and these levels are in reality historically strong, just not with the same major supply chain disruption as in 2021.

The growth agenda continues

I forecast ~£179m of revenue in FY26, ~£21m of adjusted EBIT, well above broker averages

I consider my own forecasts to be more accurate than the brokers, who cover many stocks and do not pay specific due care to Braemar. You can see that from historical forecasts from brokers which have been far behind the curve on the continuing business. At the midway of 2022, revenue forecasts for the continuing business (minus logistics) were less than £90mln and now Braemar is running at £150mln (with £10-15mln of helping hand from acquisitions).

Braemar reaffirmed broker FY24 expectations at the first half but this looks like they are setting up for an expectations upgrade later in the year on revenue. Forecasting revenue 2% down for the full year when up 8% in the first half, and when the runes suggest a significant improvement in Dry Cargo, at least stable Tankers and Risk Advisory and improved Investment Advisory does not jive with reality to me when $/£ cable is at 1.26.

After FY24, I predict Securities and the Risk Advisory unit to continue its above average growth profile. I expect this can be a £50mln revenue unit in 5-7 years, meaning out to FY26 it can grow between 15-20% per year. Investment Advisory I forecast to be a 4-8% growth unit from a lower FY24, and Chartering I conservatively forecast to be a 3-5% growth unit. I see upside on my Chartering expectations given my outlook for the overall shipping industry and ship rates as I expect Braemar’s fixtures to continue to rise.

By FY26 I see the revenue base up to £179mln with £20.9mln of underlying operating profitability, a shade higher than the £20.1mln of FY23, and contributing to nigh on £15mln of annual FCF generation. This is a business that does not have big capital expenditure needs and is working capital light in normal times. My FY25 forecast of £19.7mln of adjusted EBIT is also almost 10% above the company’s at least £18mln sustainably moving forward target.

It is no surprise that my forecasts leave me well above the broker average estimates from Investec, Edison and Cavendish. Braemar is pursuing a growth agenda and I expect shipping market conditions to mean Braemar is in for a medium haul of broker forecast upgrades. My FY25 revenue is 12% above the broker averages. I assume operating leverage gains are reinvested into the cost base to deliver further growth so on adjusted operating profit I too am 10% above and my EPS is 13% above.

My fair value target is 475p a share, which would be a 75% total return. This would be a PE ratio of 10.2x my FY26 forecast, which is not a PE ratio many investors would call stretching. Braemar will too have generated >£21mln of cumulative FCF over the rest of FY24 and FY25, which would be in part refunded to shareholders in the form of share dividends and ESOP buybacks and fuel extra M&A. This jives with Edison Research who forecast Braemar to have mounted £28m of net cash by FY26.

Stretch and ‘it went wrong’ fair value targets

My stretch target is 660p, my ‘it went wrong’ target is 200p. The easiest way for my Braemar forecasts to be wrong will be if there is a large sized swing in shipping rates beyond my own expectations. To the upside, this could drag my EPS forecast to 55p, and on this I stamp a higher 12 times PE ratio to get to 660p. This is not a high multiple but a very exuberant shipping cycle would not demand a PE ratio higher than this because it would not be sustainable. To the downside, a deep and much worse than feared macroeconomic recession could drag my EPS forecast to 25p (compared to broker averages at 37p). On this I stamp an 8 times PE ratio to get to 200p, with a lower ratio probably not fair because that would be cycle trough EPS.

Usual disclaimer!

Do your own research. I have endeavoured to be accurate and complete in my writing, but this is just a summary of my own thoughts, and my own opinions of what the company is worth and what it may deliver. Do not take this as just face value. I may have made mistakes! If you are interested, go away and come up with your own views. I would not buy or sell a stock just because I read something that someone else wrote. I would not do that for a house and I would not do that for a stock.