Elixirr can be a magical compounder

Elixirr can be a magical compounder

This challenger consultancy is on a roll growing revenue to £71m in 2022 from £26m in 2019 and EPS from 14p to 30p (108%+). There is 22%+ sales growth to come in 2023 and this looks conservative.

I hold shares in Elixirr and have since 2021 so consider me biased and DYOR

The nutshell: Elixirr has demonstrated its compounding abilities already, the stock is 121%+ on its ipo price but the 480p level now offers great value for investors and much better value than the 770p peak price of April 2022. The 2024 price/earnings prospective ratio is now only 13.3x for a company run-rating growth at well over 20% organically, superb 25%+ operating profit margins and while cash balances (zero debt) are forecast to swell to £46.4m, 21% of today’s market value. Broker fair value 959p. My fair value is 850p.

If you want to watch a compelling company presentation → https://www.investormeetcompany.com/investor/meeting/investor-presentation-203

Where did Elixirr come from? How many companies had the balls and the business story to sell to investors with an ipo during 2020 with the coronavirus pandemic? Hard;y many is the answer, but on 9th July 2020 Elixirr started trading on the AIM market marking the first IPO on the market since the start of the UK lockdown due to COVID-19. Elixirr was founded in 2009 (yes, in the depths of the GFC) by Stephen Newton who remains a hugely aligned 29% shareholder today. It was founded by 4 ex-Accenture consultants and an ex-Magic Circle lawyer who wanted to disrupt the enormous, but traditional, consulting industry with a more differentiated approach. At the point of IPO Elixirr had produced a whopping 32% sales CAGR since 2012, and the CAGR since 2019 has been 39% with high profit margins.

Elixirr’s 3 competencies: Elixirr has three business areas;

Management consulting (think the relevant business units in Deloitte, EY, KPMG); business strategy, corporate innovation, risk and compliance, procurement, target operating model

Elixirr Digital (think Publicis Sapient); Digital strategy, brand strategy, digital design, digital optimisation

Technology & Data (think Accenture, Globant); data strategy, AI and machine learning, application design and development, IT strategy

Sample of some of Elixirr’s customers

What is the secret growth sauce? Elixirr is twin-running a strong organic growth platform with a buy and build strategy, bringing in motivated management teams on their own platforms into the Elixirr stable. So far this has included US data and technology consultancy iOLAP, digital marketing firm Coast Digital, digital agency Den Creative and procurement consultancy Retearn. Elixirr has a very entrepreneurial culture with aligned partners. They also think about results and not billable hours with a pricing model that reflects that fees are aligned to client goals. At the time of IPO an independent 2019 survey showed that clients rated Elixirr 8.6/10 for overall performance, 32% higher than competition.

What is the opportunity? Elixirr is tackling large addressable pools of spend locked down today by the big guns like Deloitte, PWC, EY, KPMG, McKinsey and more technology pinnacled Accenture. If I only take the consulting revenue from 2021 the market total was $234 billion of spend and had been growing at 8% per year so at £71m of revenue in truth Elixirr is merely surface scratching and has a lot of leg room. Areas of digital and also data and AI that iOLAP brought in are the most exciting areas, but don’t forget that even the heritage management consulting business is a strong organic compounder (and has to be!) when the business is run-rating 29% organic growth so far in 2023.

Earnings upgrades galore: For me this is the killer graphic. Elixirr is a serial upgrader of expectations caused by organic growth outperformance and accretive acquisitions. Upgrades from start to finish were 9% for FY20, 42% for FY21, 58% for FY22, 41% for FY23, and are already running at 12% for FY24.

More earnings upgrades will come: Elixirr has given guidance for 2023 just a few weeks ago. Organic growth is accelerating with January a record month and organic growth of 29%. Elixirr say “Expectations for full year FY23 are for revenue of £85-87m with Q1 currently trading ahead of this.” In other words they are yet again organically outperforming, Finncap have in just 14% organic growth for 2023 and I can see Elixirr doing ahead of 20% for the year overall. Then we can talk about M&A. Elixirr already has £20.4m of net cash to play with and this is forecast (thanks to great cash generation) to £46.4m by the end of FY23, this upgrade train can keep on rollin’. If I take 4-6x EBITDA multiples upfront from the last 2 deals and say they spend £30m on new deals then that is another £5m to £7.5m of M&A accretion to come. That alone is 21% to 32% accretion off the forecast 2023 EBITDA figure. I would peg to 6x but market multiples have fallen off over the last 2 years. Elixirr call out a strong M&A pipeline subject to a rigorous and disciplined diligence process.

CEO Stephen Newton in the recent trading update: Stephen Newton, CEO of Elixirr, said: "Elixirr delivered growth on all key metrics during FY22. It was particularly pleasing to see the improved value creation from using all four pillars to grow our firm - it is the year that brought our IPO thesis (coupling organic and inorganic growth) to life. The turbulent macroeconomic backdrop and our strategic purchases have made Elixirr's services even more relevant at a board level as we help our clients to navigate the changing business environment. The momentum we have delivered in 2022 is accelerating in 2023, and we expect further growth across all our pillars as the year progresses."

Forecast to grow at almost double the rate of Accenture at a 34% discount: Finncap point out that their 3 year operating profit growth CAGR for Elixirr is 20.2%, and this will be bumped further by any M&A deals. In comparison Accenture’s operating profit number is 10.5%. Accenture is on a price earnings multiple of 20 for 2024 while Elixirr is only on 13.3x and Elixirr will have far more cash/market value than Accenture. Boy, what a stock Accenture has been, a quality compounder itself with an inorganic and organic approach.

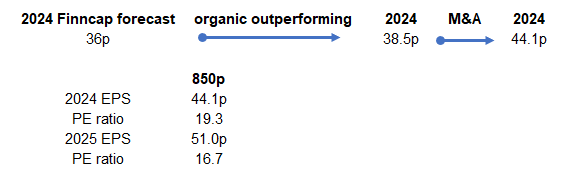

Getting to 850p: My 850p fair value is bullish but I think very real and even if I am wrong there is large upside from 480p today. I expect 2024 eps to come in at 44.1p, 22% higher than the current Finncap forecast and 37% higher than Finncap’s first FY24 forecast. If you think this is too bullish look back at the earnings upgrades in the years before and this looks achievable.

Price/earnings multiple round tripped to highly attractive bottomed levels: Elixirr has long been valued highly and rightly so, but with the market correction investors have waxed and waned in many stocks and this is one. I plotted the forward PE of Elixirr at each Finncap report to show this. The stock is as cheap as at ipo when the stock market had been brutalised and before Elixirr has demonstrated another 2 years of excellent performance. Finncap have a 959p price target on the stock.

Big long term ambitions: CEO Stephen Newton wants to see the past growth rates maintain going forwards and he wants to take on McKinsey in particular. Starting at 2023, the ambition is to continue to grow strongly, 30% being baseline and 25% being conservative, and looking to reach a $1bn market cap business by 2028. At my 850p target the market valuation would be close to $0.5bn and halfway there.

Hey Harry! Thank you for your write-up! Wish you the best!